Considering Performance Stock Options

Key Takeaways

- Executive pay package stock options have fallen in prevalence and prominence over the past 15 years, having been replaced primarily by long-term, performance-vested stock plans.

- Many companies struggle to set rigorous yet fair long-term performance goals or define an appropriate peer group against which to measure relative TSR.

- Setting appropriate performance goals is critical for performance share and similar plans because full vesting results in executives realizing the targeted number of shares at their current value.

- Performance-vested stock options simplify long-term performance goal setting because gains realized by executives require both satisfaction of the performance vesting conditions and increases in company share price. Vesting by itself does not guarantee any gain, and gains are scaled not to competitive pay targets but to increases in shareholder value. This enhanced shareholder alignment makes setting rigorous performance goals less critical than it is for performance share and similar plans.

- The characteristics of performance options may make them the best fit in many situations.

- As such, companies should consider them when evaluating long-term performance plan design alternatives.

Background

The rise in both the prevalence and prominence of long-term performance plans has been one of the most significant trends in executive compensation over the past 15 years. At the time of the dot-com market collapse (March 2000 to October 2002) and the demise of several prominent U.S. companies (e.g., the Enron scandal revealed in October 2001), long-term performance plans were only used by a relatively small portion of large U.S. public companies. Today, more than 80% of S&P 500 companies use a variety of LTI performance plans, including performance shares, performance units, performance-vested restricted stock and/or units, and long-term cash-based incentives. More striking than the growth in prevalence of long-term performance plans is the increased prominence of performance plans in the mix of LTIs provided by companies. Long-term performance plans now represent approximately 52% of CEO total LTI compensation opportunities.1

The increased prevalence and prominence of long-term performance plans have come primarily at the expense of stock options. Corporate America began using stock options in executive pay packages in the 1950s, with use peaking during the late 1990s tech boom and bull market for stocks. Today, even though stock options are granted to 54% of S&P 500 CEOs, they typically represent only 18% of CEO total LTI award value.1

In our judgment, stock options have declined in popularity for 3 major reasons:

- In the early 2000s, several large companies ” including Enron and WorldCom ” collapsed due to fraudulent business practices linked to the extensive use of stock options. As a result, stock options were given a “black eye” by the business press and frequently cited as motivating unhealthy ” if not unethical ” practices to pump up short-term results at the expense of long-term sustainable gains in shareholder value.

- In 2006, the accounting profession mandated a major change to the accounting treatment of stock options. For the first time, accountants required a direct charge to earnings for the grant of stock options, eliminating the comparatively advantageous accounting treatment afforded options for more than half a century.

- In 2010, the SOP shareholder advisory vote on executive compensation ” included by Congress as part of the Dodd-Frank Financial Reform Act ” greatly enhanced the influence of proxy advisory firms. Some proxy advisors have taken the position that a typical stock option (i.e., with a strike price equal to the company share price at grant and exercise rights vesting over time) is not performance-based compensation. Instead, proxy advisors advocate long-term performance plans that vest or pay out based upon achievement of nominal or relative performance measures. A sufficient number of institutional investors have supported this view, causing many companies to feel pressured to grant >50% of LTIs in the form of such performance-vested awards.

The Challenge of Setting Long-Term Goals

One appealing feature of stock options is that they do not require the company to set performance goals. However, the initial P4P paradigm that emerged to replace stock options tied vesting and payouts to the achievement of long-term goals for company operating results. Such long-term performance plans are essentially an extension of annual incentive plans by rewarding executives for achievement of targeted operating results over several years. Setting rigorous but fair long-term goals for ~3 years has proven difficult, if not impossible, for many companies for a variety of reasons (e.g., results tied to commodity pricing trends, new technological or product breakthroughs, new government rules and regulations, and the underlying health of the economy). As a result, payouts from long-term performance plans are often perceived to be substantially attributable to long-term goals that were set too high or too low. The Challenges of Relative TSR To avoid the problems associated with setting long-term goals, many companies have returned to stock price as the preferred measure of company performance but with a twist: the change in company value, measured as change in stock price plus dividends (TSR), is compared on a relative basis to the TSR of “peer companies.” The relative TSR concept is that management’s performance in running the company is reflected in any premium or deficit in TSR versus its peers. Despite this intuitively attractive P4P paradigm, measurement problems for relative TSR plans abound, such as:

- some companies do not have a logical peer group of companies that compete in the same industry segments and experience the same economic conditions which facilitate or limit growth and profitability opportunities;

- relative TSR performance can be attributable to peer company performance as well as plan sponsor company performance; and

- share prices often move for reasons that are not directly connected to performance. For example, economists estimate that at any point in time, >50% of a share’s price is determined by factors beyond company performance. Some of these factors are common to all stocks, such as the discount rate for capitalizing future earnings, but other factors may be specific to an industry subset or a particular company, such as M&A expectations.

Performance Stock Options (PSOs)

Companies that have struggled with these P4P paradigms may be overlooking an alternative that could better fit their situation: PSOs. A PSO is an option that vests on achievement of operating goals, share price goals, or a combination of both. The case for performance options can be summarized as follows:

Performance options use the familiar stock option vehicle to reduce the challenge of setting long-term performance goals, and the risk of setting unfair goals, while delivering payouts that are completely aligned with shareholders.

How do PSOs reduce the challenge of setting long-term goals? PSOs require an increase in share price to generate realizable gains on exercise, and so the risk of vesting and paying out large gains for achieving “easy” goals is greatly diminished. In contrast, rigorous goals are considered essential to PSU awards due to the large gains that are immediately realized upon vesting.

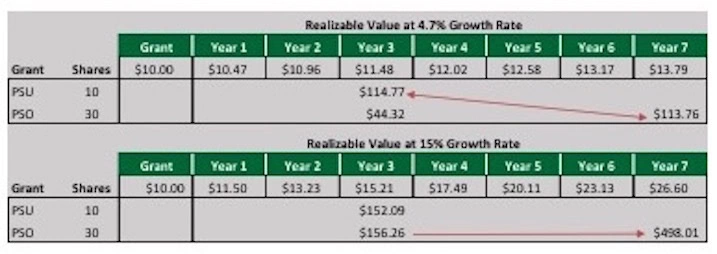

This critical difference is illustrated below by comparing the potential realizable values of PSUs and PSOs. The illustrations assume that the awards are made at $10 fair market value, that 3 PSOs with a 7-year term have the same grant value as 1 PSU, and that both PSUs and PSOs vest at target. The illustrations show that:

- For low share price growth rates (4.7% or less), PSUs provide more realizable value after year 3 than do PSOs after year 7.

- At a 15% share price growth rate, PSOs provide similar realizable value as PSUs after year 3 but offer far greater upside opportunity in subsequent years if high share price growth continues.

The illustrations also indicate that for share price growth rates between 4.7% and 15%, PSOs require 4 to 7 years to provide a similar realizable value as PSUs after year 3.

Arguably, PSOs are more “shareholder friendly” than PSUs in several respects:

- PSOs provide gains to executives in proportion to gains realized by shareholders (i.e., a significantly lower realizable value at low share price increases, and a significantly higher realizable value at higher share price increases). In contrast, a company issuing PSUs could achieve its operating goals ” or rank high on relative TSR ” but still have a very low TSR for shareholders while paying out target or greater gains to executives.

- The performance orientation of PSOs is generally longer than that of a typical 3-year PSU due to the time required to generate gains and the 7 or 10-year term for exercising them.

- Because vesting of PSOs is no guarantee of significant gains, shareholder concerns over vesting goals should be diminished, and companies can set goals with less “stretch” than what is expected for PSUs.

An analogy to setting less “stretch” in goals can be found in RSU awards that generally vest over time but also require that a specified level of performance be achieved as a precondition to the time vesting. This design is used to qualify the RSUs for a company tax deduction under IRC 162(m). Shareholders, shareholder advisors, and the IRS have viewed many such plans as “performance based” and qualified for a tax deduction so long as there is a significant risk associated with achieving the performance criteria for vesting. Tax qualification isn’t generally an issue for stock options with an exercise price set at grant date fair market value: the IRS presumes they are performance based. However, this recognition from shareholders and their advisors is important to shareholder relations and SOP voting.

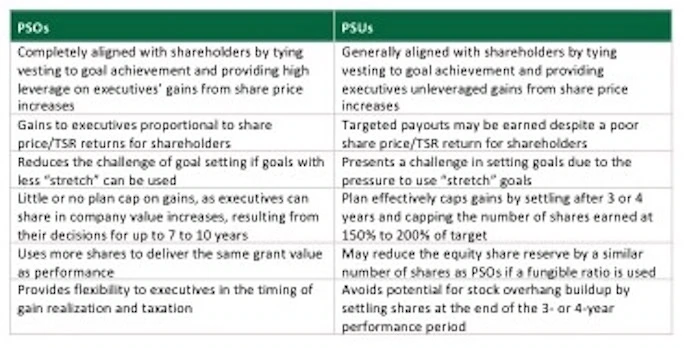

Performance Options versus Performance Shares

Considerations in selecting PSOs or PSUs are highlighted in the table below.

When Should Performance Options Be Considered?

Performance options are more likely to be a good fit in the presence of one or more of the following:

- high degree of difficulty in setting long-term financial goals;

- ability to set long-term financial goals but not necessarily the timing of achievement;

- poorly-fitting or nonexistent peer group or index for comparing relative results;

- competitive pressure to grant stock options but it needs performance vesting to secure strong shareholder support;

- desire to motivate and reward “transformational” changes in the company through a special, one-time grant; or

- desire to provide uncapped upside gains proportional to increases in company market capitalization.

PSOs that are properly understood and designed may provide the best fit for many companies. They should be considered whenever companies evaluate long-term performance plan design alternatives.

____________________________________